The refinance definition refers to the process of replacing an existing loan with a new one, usually with better terms, a lower interest rate, or a different repayment structure. Understanding the refinance definition is important for homeowners, borrowers, and anyone managing debt, as refinancing can significantly impact financial planning and long-term savings.

In simple terms, the refinance definition involves taking out a new loan to pay off an old loan, often to reduce monthly payments or save money on interest over time.

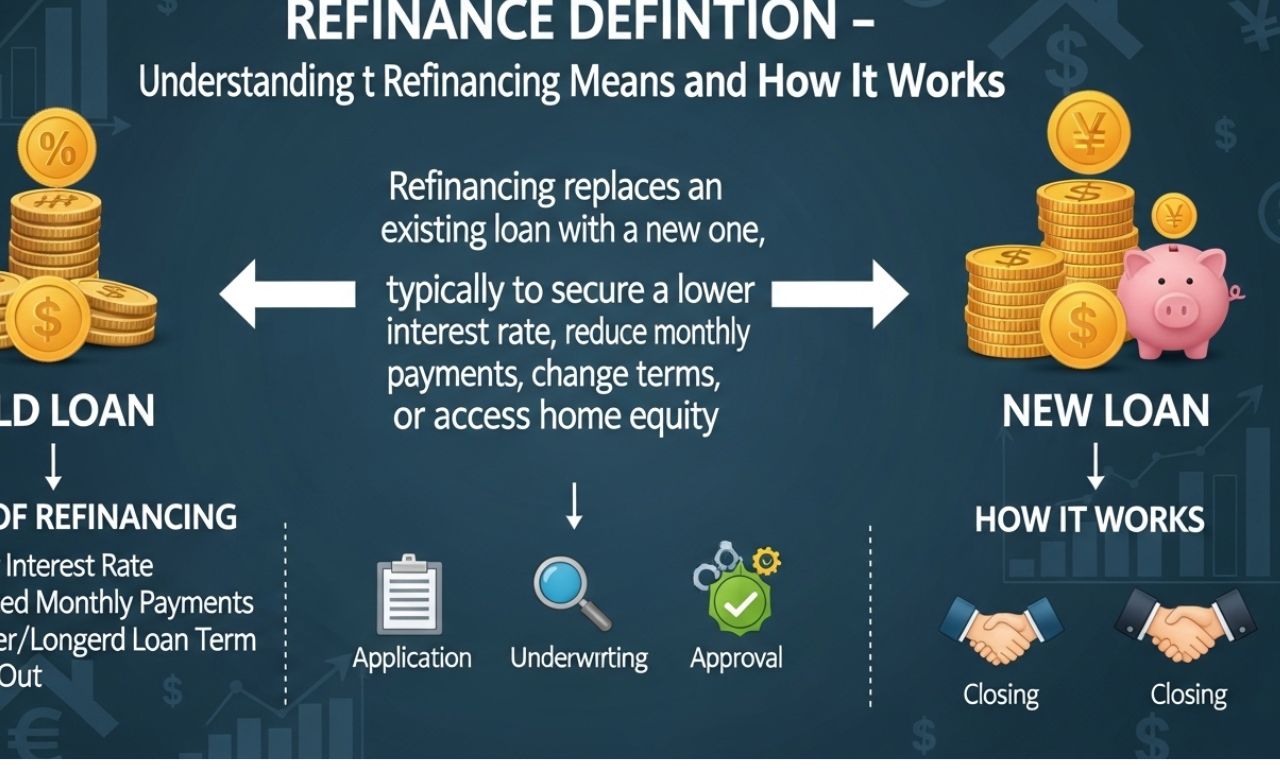

What is the Refinance Definition?

The refinance definition can be described as the act of revising and replacing the terms of an existing loan agreement. This is commonly done with mortgages, but refinancing can also apply to auto loans, student loans, and personal loans.

When you refinance, a new lender (or sometimes the same lender) pays off your existing loan and creates a new loan with updated terms. The goal is often to improve financial conditions such as:

- Lower interest rates

- Reduced monthly payments

- Shorter or longer loan terms

- Switching from variable to fixed interest rates

This makes the refinance definition an important financial strategy for managing debt more effectively.

How Does Refinance Work?

To better understand the refinance definition, it is helpful to know how the process works:

- Apply for a new loan – You apply with a lender for refinancing.

- Loan approval – The lender reviews your credit, income, and financial history.

- New loan terms – If approved, you receive new loan terms, which may differ from your current loan.

- Pay off old loan – The new loan is used to pay off your existing loan.

- Begin repayment – You start making payments on the new loan under the revised terms.

This process allows borrowers to replace unfavorable loan conditions with better ones, aligning with the core refinance definition.

Types of Refinancing

There are several types of refinancing options that help explain the broader refinance definition:

1. Rate-and-Term Refinance

This is the most common type of refinancing. It involves changing the interest rate, loan term, or both without borrowing additional money.

2. Cash-Out Refinance

With this option, you borrow more than you owe on your current loan and receive the difference in cash. This is often used for home improvements or debt consolidation.

3. Cash-In Refinance

In this case, the borrower pays a lump sum to reduce the loan balance and qualify for better terms.

4. Streamline Refinance

This is a simplified refinancing process that requires less documentation and is often available for government-backed loans.

Each type supports the overall refinance definition by offering different ways to restructure existing debt.

Benefits of Refinancing

Understanding the refinance definition also involves recognizing its benefits:

- Lower interest rates: Reduce the total cost of borrowing

- Reduced monthly payments: Improve cash flow

- Shorter loan term: Pay off debt faster

- Debt consolidation: Combine multiple debts into one payment

- Access to cash: Use equity for important expenses

These advantages make refinancing a popular financial strategy for many borrowers.

Risks and Considerations

While the refinance definition includes many benefits, there are also risks to consider:

1. Closing Costs

Refinancing often comes with fees such as appraisal costs, origination fees, and closing costs.

2. Longer Loan Terms

Extending your loan term may lower monthly payments but increase total interest paid over time.

3. Credit Impact

Applying for refinancing can temporarily affect your credit score.

4. Break-even Point

It may take time to recover the costs of refinancing, so it is important to calculate whether it is financially beneficial.

These factors are essential when evaluating whether refinancing aligns with your financial goals.

When Should You Consider Refinancing?

Based on the refinance definition, refinancing may be a good option in the following situations:

- Interest rates have dropped significantly

- Your credit score has improved

- You want to lower monthly payments

- You want to pay off your loan faster

- You need access to cash through home equity

If these conditions apply, refinancing could help you achieve better financial outcomes.

Example of Refinance in Practice

To better understand the refinance definition, consider this example:

Suppose you have a mortgage with a 7% interest rate. If market rates drop to 5%, refinancing allows you to replace your existing loan with a new one at 5%. This reduces your monthly payments and saves money over the life of the loan.

This practical example shows how refinancing works in real-world situations.

Refinance Definition in Mortgage Loans

In the context of home loans, the refinance definition is most commonly applied to mortgage refinancing. Homeowners refinance to:

- Lower their interest rate

- Switch loan types

- Tap into home equity

- Adjust payment schedules

Mortgage refinancing is one of the most widely used financial strategies under the refinance definition.

Tips for Successful Refinancing

To make the most of refinancing, keep these tips in mind:

- Compare multiple lenders before choosing

- Check your credit score before applying

- Calculate total costs vs. savings

- Consider your long-term financial goals

- Read all terms carefully before signing

Following these steps ensures that refinancing aligns with your financial situation.

Conclusion

The refinance definition is centered around replacing an existing loan with a new one to achieve better financial terms. Whether you are lowering your interest rate, reducing monthly payments, or accessing cash, refinancing can be a powerful financial tool when used wisely.

Understanding the refinance definition, along with its benefits and risks, allows borrowers to make informed decisions that improve their financial health and long-term stability.