Understanding a mortgage becomes easier once the parts of the payment feel familiar. Many homeowners start out unsure about how lenders separate the amount that reduces the loan from the amount that reflects the cost of borrowing. Clarity grows once the basic structure is explained in plain language.

The concept behind how to calculate principal and interest on a mortgage shapes every monthly payment. It influences how quickly the balance falls and how much the loan costs over time. Knowing the way each portion works creates a sense of control that supports clear decisions.

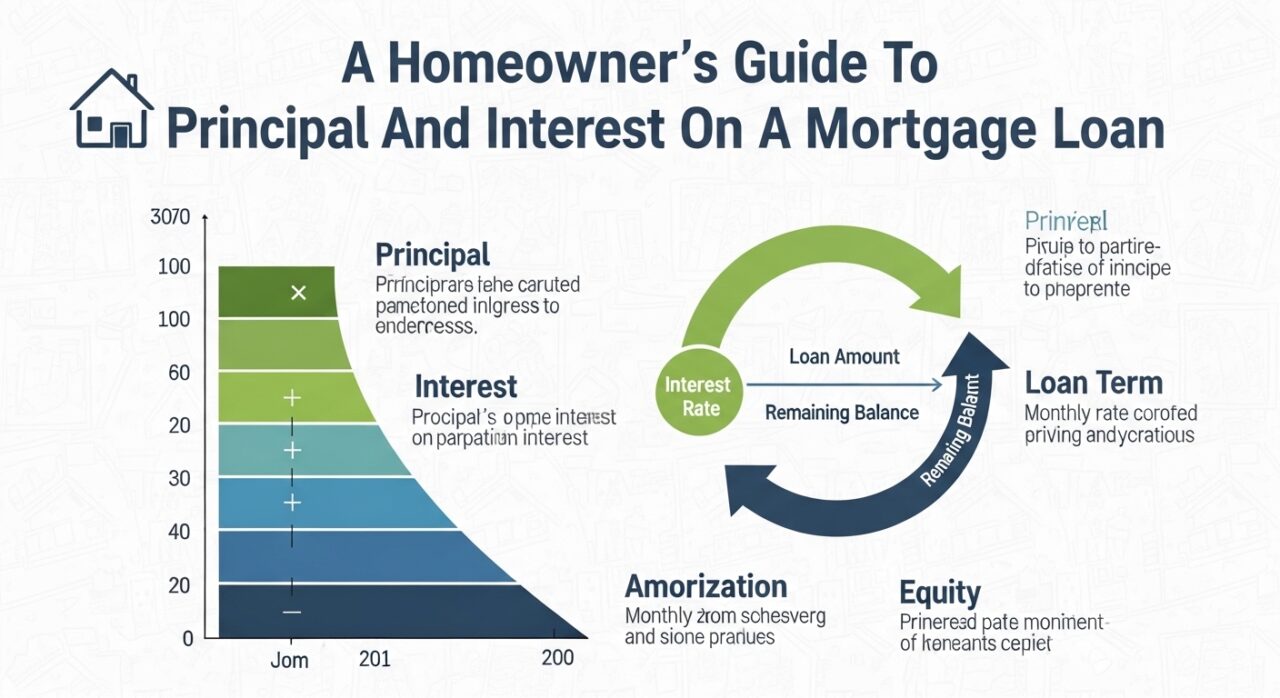

How Principal Works In A Standard Mortgage

Principal represents the actual amount borrowed. It moves downward each time a payment is made, though the early decrease may look small. The pace changes as the loan matures, since later payments contain a larger slice directed to the balance. It becomes a steady path of gradual reduction.

Understanding principal brings helpful perspective. Homeowners see how extra payments can trim the balance at a quicker pace. A clearer view of principal shows the real progress behind each month’s effort. It also helps set expectations for how the loan behaves in different stages.

How Interest Fits Into Each Payment

Interest functions as the cost of borrowing. Lenders calculate it based on the outstanding balance, so larger amounts early in the loan create higher charges. As the balance decreases, interest takes a smaller portion of the monthly payment. The shift becomes noticeable once the loan has aged.

Interest plays a key role in planning. Homeowners benefit from knowing how the amount changes as the loan moves through its schedule. That knowledge creates a more grounded sense of timing and budgeting. It also supports a practical view of how payments shape total cost.

The Formula Behind Standard Calculations

Mortgage calculations rely on a clear formula that blends rate, term, and original balance. Lenders use an amortization structure that determines how each payment is divided. This system places more interest in the early years and more principal later. The pattern helps maintain stable monthly payments.

Seeing the formula in action makes the math feel less mysterious. An online calculator or lender’s tool reveals the breakdown for each month. It offers a simple way to understand how rate changes or different terms influence payment size. The formula becomes a guide that helps homeowners compare options.

Factors That Influence Payment Behavior

Rates have a strong influence on interest. Even small shifts can alter the cost of borrowing, which affects the payment split. A fixed rate holds steady while a variable rate adjusts according to market conditions. Each structure shapes how the loan behaves over time.

Loan term also plays a noticeable role. Shorter terms compress repayment and increase monthly obligation, while longer terms stretch repayment and create smaller payments. Each choice changes the progression of principal and interest. Homeowners select based on comfort, goals, and personal pace.

Understanding how to calculate principal and interest on a mortgage strengthens financial awareness. It builds confidence in decisions and reduces uncertainty around monthly payments. A clearer picture of principal and interest shows how each part contributes to progress. This understanding supports practical planning that aligns with personal goals. A homeowner who grasps these basics moves through repayment with a steady sense of direction.