In the world of investing, the term alpha is widely used to measure the performance of a portfolio or investment relative to a benchmark index. Investors, fund managers, and financial analysts often track alpha to understand whether an investment is generating excess returns beyond what is expected based on its risk level. Understanding alpha can help investors make more informed decisions about their portfolios and evaluate the skill of fund managers.

Definition of Alpha in Finance

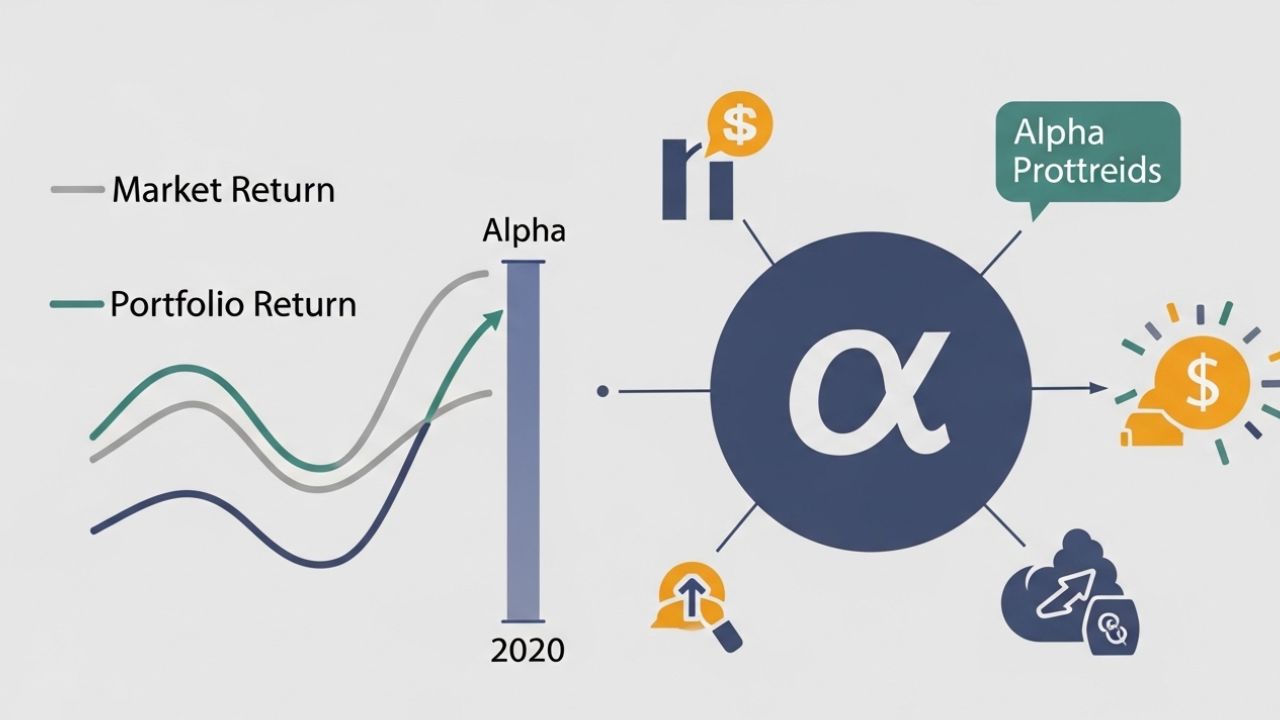

In finance, alpha (α) represents the excess return of an investment relative to the return of a benchmark index. It shows whether an investment has outperformed or underperformed compared to the market or a specific benchmark.

- Positive Alpha (>0): The investment has outperformed the benchmark.

- Negative Alpha (<0): The investment has underperformed the benchmark.

- Zero Alpha (0): The investment’s performance is in line with the benchmark.

Mathematically, alpha is often expressed as:

α=Ri−[Rf+β(Rm−Rf)]\alpha = R_i – [R_f + \beta (R_m – R_f)]

Where:

- RiR_i = Actual return of the investment

- RfR_f = Risk-free rate of return

- β\beta = Beta of the investment (sensitivity to market movements)

- RmR_m = Return of the benchmark market index

How Alpha Is Used in Investing

Alpha is a key metric in portfolio management and investment analysis:

1. Evaluating Fund Managers

Investors use alpha to determine how well a fund manager has performed relative to the market. A high positive alpha suggests the manager has added value through stock selection and timing.

2. Comparing Investments

Alpha helps compare two similar investments by showing which one has delivered better risk-adjusted performance relative to the benchmark.

3. Risk-Adjusted Performance

Unlike raw returns, alpha accounts for the risk taken to achieve the return. It works alongside beta, which measures volatility, giving a complete picture of investment performance.

Examples of Alpha in Finance

- Positive Alpha Example:

Suppose a mutual fund delivers a 12% return over a year, while its benchmark index returned 8%, and the fund’s beta-adjusted expected return was 9%. The alpha would be:

α=12%−9%=3%\alpha = 12\% – 9\% = 3\%

This means the fund outperformed expectations by 3%.

- Negative Alpha Example:

If the same fund only returned 7% while the expected return based on risk and market performance was 10%, the alpha would be:

α=7%−10%=−3%\alpha = 7\% – 10\% = -3\%

This indicates underperformance relative to risk-adjusted expectations.

Alpha vs Beta

While alpha measures excess return, beta measures market-related risk:

- Alpha: How much return an investment generates beyond its expected performance.

- Beta: How sensitive the investment is to overall market movements.

Together, alpha and beta provide a comprehensive view of risk-adjusted performance.

Limitations of Alpha

Although alpha is an important metric, it has some limitations:

- Benchmark Dependence: Alpha is only meaningful relative to the chosen benchmark. A poorly chosen benchmark can give misleading results.

- Short-Term Fluctuations: Alpha can vary significantly over short periods and may not reflect long-term performance.

- Doesn’t Capture All Risks: Alpha considers market risk via beta but may ignore other risks like liquidity, credit, or geopolitical factors.

Why Alpha Matters for Investors

Investors rely on alpha to:

- Identify outperforming funds or stocks

- Measure active management skills of fund managers

- Make risk-adjusted investment decisions

- Optimize portfolio performance for long-term growth

A consistently positive alpha is often a sign of a well-managed, skillful investment strategy.

Conclusion

In finance, alpha is a crucial metric that indicates the value added by an investment relative to its risk-adjusted benchmark return. Whether you are a casual investor or a professional portfolio manager, understanding alpha can help you assess performance, compare investment options, and make smarter financial decisions. While it should not be the only measure used, alpha offers insight into excess returns and fund management effectiveness.