If you’ve ever wondered, “what are tranches in finance?”, you’re not alone. Tranches are an essential concept in structured finance, used to divide complex financial products into multiple segments with different levels of risk, return, and priority. Commonly found in mortgage-backed securities, collateralized debt obligations, and other pooled investments, tranches allow investors to choose the level of risk they are comfortable with while providing issuers flexibility in structuring loans or securities. This article explains tranches in finance, how they work, the different types, and their implications for both investors and issuers.

Understanding Tranches in Finance

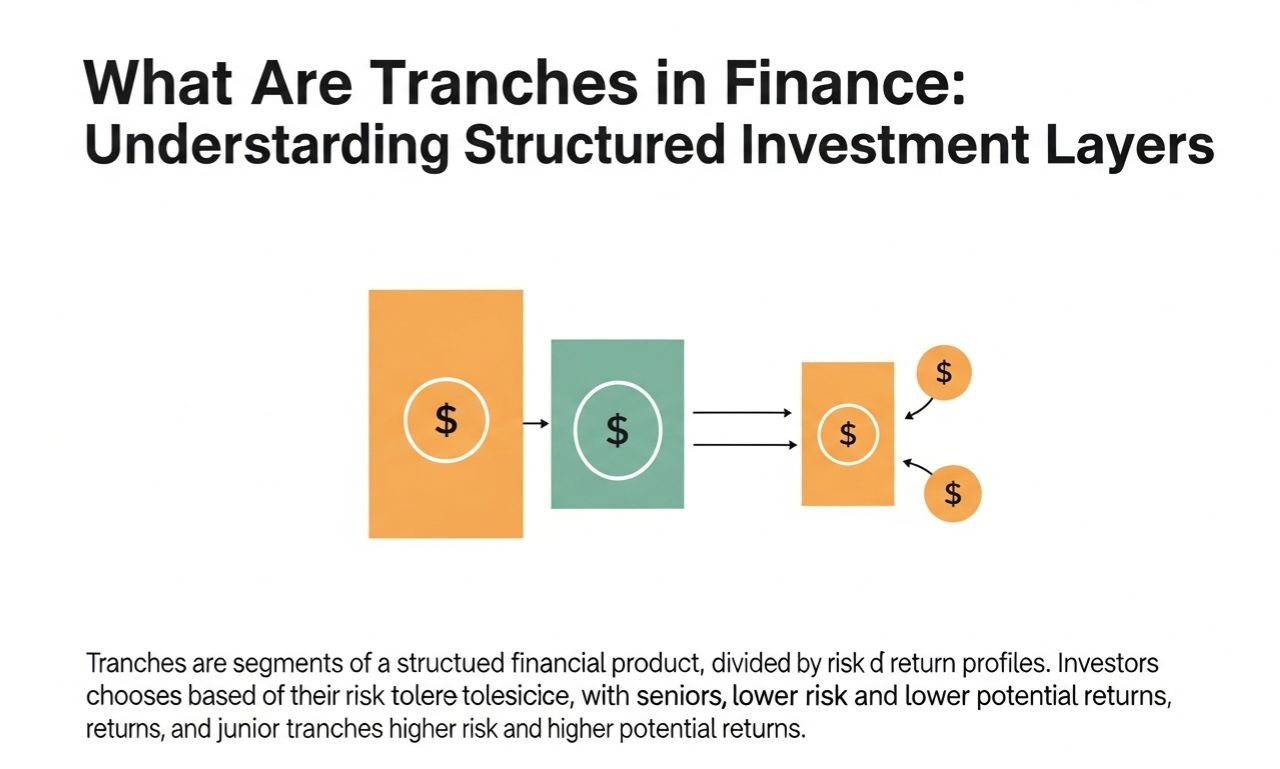

Definition of Tranches

In finance, a tranche is a portion or slice of a structured financial product. Each tranche represents a separate class of debt or security with distinct characteristics, including risk, maturity, and interest rates. By creating tranches, issuers can appeal to different types of investors, from those seeking safe, low-yield investments to those willing to take higher risks for potentially higher returns.

Purpose of Tranching

Tranching allows issuers to:

-

Attract a wide range of investors with varying risk appetites.

-

Optimize financing costs by offering lower interest rates for senior, low-risk tranches.

-

Distribute cash flows efficiently among investors according to their tranche’s priority.

How Tranches Work

Structure of a Tranche

Tranches are typically structured in a hierarchy:

-

Senior Tranche:

-

Lowest risk and priority for repayment.

-

Receives interest and principal first.

-

Usually has the lowest yield due to lower risk.

-

-

Mezzanine Tranche:

-

Medium risk and repayment priority.

-

Higher interest rates than senior tranches.

-

Acts as a buffer between senior and junior tranches.

-

-

Junior or Equity Tranche:

-

Highest risk and last in line for repayment.

-

Potential for the highest returns.

-

Often absorbs losses first if the underlying assets underperform.

-

Cash Flow Distribution

Cash flows from the underlying assets, such as loan payments or mortgage collections, are distributed according to tranche hierarchy. Senior tranches are paid first, mezzanine next, and junior last. This structure protects lower-risk investors while offering higher potential returns to those accepting more risk.

Types of Tranches

Mortgage-Backed Security (MBS) Tranches

MBS tranches are slices of pooled mortgages. Investors can choose senior, mezzanine, or junior tranches based on risk tolerance. Senior tranches are less likely to face defaults, while junior tranches may experience higher volatility but higher potential gains.

Collateralized Debt Obligation (CDO) Tranches

CDOs pool corporate bonds, loans, or other debt. Each tranche carries different risk and return profiles. The tranche structure allows banks and investment firms to repackage and sell debt to investors, spreading risk across multiple levels.

Collateralized Loan Obligation (CLO) Tranches

CLOs are structured finance products backed by corporate loans. Tranches allow different investors to participate, from conservative institutions seeking stable returns to hedge funds looking for high-risk, high-reward opportunities.

Advantages of Tranches in Finance

Risk Management

Tranches allow risk to be allocated according to investor preference. Senior investors take lower risk, while junior investors assume higher risk but have the potential for greater returns.

Access to Investment Opportunities

By dividing complex products into tranches, smaller investors can participate in large-scale investments that would otherwise be inaccessible.

Customization of Returns

Tranches enable issuers to offer varying interest rates, maturities, and cash flow structures, making products attractive to different types of investors.

Risks Associated With Tranches

Credit Risk

Junior tranches are exposed to higher default risk. If the underlying assets perform poorly, investors in these tranches may lose their principal.

Complexity Risk

Structured products with multiple tranches can be complex and difficult for some investors to fully understand. Poorly informed investment decisions can lead to unexpected losses.

Market and Liquidity Risk

Tranches, especially lower-rated ones, may be harder to sell in the secondary market, which can impact liquidity and investment flexibility.

Real-World Examples of Tranches

The 2008 Financial Crisis

Tranches in mortgage-backed securities played a significant role in the 2008 financial crisis. Senior tranches were initially considered safe, while junior tranches carried higher risk. When housing defaults increased, even some senior tranches suffered losses, demonstrating the importance of understanding underlying asset quality.

Modern Use

Today, tranching is used in corporate finance, securitization, and investment products. Banks, insurance companies, and investment firms use tranches to structure loans, bonds, and asset-backed securities to meet specific risk and return goals.

How Investors Can Approach Tranches

Assess Risk Tolerance

Investors should choose tranches based on their willingness to accept risk. Conservative investors typically select senior tranches, while those seeking higher returns may consider mezzanine or junior tranches.

Analyze Underlying Assets

The performance of tranches depends on the quality of the underlying assets. Conduct thorough due diligence on mortgages, loans, or bonds backing the tranche before investing.

Diversify Across Tranches

Spreading investments across different tranches can help balance risk and return, reducing exposure to a single level of risk.

Conclusion

Understanding what are tranches in finance is essential for anyone involved in structured investments, mortgage-backed securities, or collateralized debt obligations. Tranches allow issuers to distribute risk and returns strategically, while investors can select the level of risk that aligns with their financial goals. While tranches offer advantages like risk management, access to large-scale investments, and customizable returns, they also carry complexities and potential risks. By carefully analyzing the underlying assets and tranche structure, investors can make informed decisions and participate effectively in the world of structured finance.